An open letter to political leaders written by investment management firm Letko Brosseau, ‘LB’, signed by about ninety current and former Canadian corporate chief executive officers, exhorts government officials to induce public pension plans to allocate more – apparently, much more – of their invested assets in public and private Canadian stocks and debt.

LB notes that pension funds have legislated advantages, including non-taxability. So, in LB’s argument, governments should help capital-starved enterprising firms by either encouraging or compelling the investing of more capital from monies entrusted to fund managers. These managers control over a trillion dollars in assets, so this would be very consequential.

This idea may be initially appealing, but, if enacted, would bring higher risks, poor returns, and even an inability to meet guaranteed benefits. The colossal inflated costs of government-controlled projects, such as the TransMountain Pipeline, hydroelectric plants such as Manitoba’s Keeyask, and Newfoundland and Labrador’s Muskrat Falls, are discouraging.

Even if fund managers avoided dubious ‘opportunities’ such as those, Canada’s equity markets are not as enticing as LB and friends indicate. LB states that Canadian pension fund managers’ Chinese investments, now CAD$88 billion, exceed the $81 billion in Canada. However, China’s stock market is far larger than Canada’s (at USD$10.9 trillion, versus Canada’s under CAD$3.6 trillion, and that after excluding foreign companies and exchange-traded funds).

While investing in the capriciously ruled People’s Republic of China is questionable, prudent fund managers lower their risk and improve returns by carefully investing internationally – where there is a low correlation to domestic markets, or as to contain opportunities missing domestically.

Furthermore, the investment ‘universe’ of global regions and asset types (including stocks, bonds, mortgages, private equity and debt, infrastructure, royalty streams, commodities, and real estate) is huge. Canadian stocks are just 2.5% of global total market capitalization. Hence, funds naturally buy into industries, companies and nations that have different or lower risks, and seek higher potential returns than those available in Canada.

According to a Globe and Mail article, ‘passively’ investing in the U.S. Standard & Poor’s 500 stock index over the past fifteen years (ending February 28th.) generated a total return (dividends reinvested) of 825%, versus the TSX Composite Index’s 310%. Canada’s stock markets’ minor presence in high-growth industries compared to United States and elsewhere lowers overall returns. Some examples: semiconductors, robotics, artificial intelligence, software, cloud computing, scientific, and technical instruments, biotech, medical devices, video and computer games, aerospace and defence.

‘Tilting’, as LB suggests, more capital into Canadian miners, oil companies, retailers, banks and financial firms will neither foster an ‘economy of tomorrow’, nor cure Canada’s productivity issues and lacklustre investor appeal. Promising firms already attract abundant venture capital money ($6.9B in 660 deals in 2023 alone, plus billions through junior stock exchanges: TSX Venture, CSE, Neo).

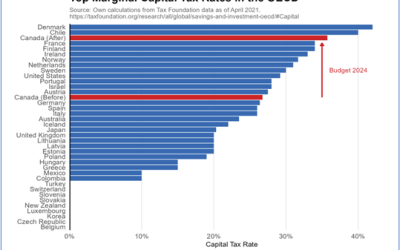

Shopify, AbCellera, General Fusion and D-Wave are Canadian examples of innovative, well-managed firms which always attract investors. Raising the capital gains inclusion rate to 2/3 from ½ in the latest budget is typical of Ottawa’s ignorance of what does and does not make investing here alluring. Inducing portfolio managers to violate their standards and risk beneficiaries’ future benefits – that of regular Canadian citizens – is a high price to steer more so-called ‘cheap’ capital to firms that cannot attract it otherwise.

Ian Madsen is the Senior Policy Analyst at the Frontier Centre for Public Policy